In today’s competitive market, exceeding client expectations goes beyond exceptional service; it involves strategically using financial insights to fuel growth and drive business success. Our very own Jason Kruger, Founder and CEO of Signature Analytics, delves into these key financial strategies on the latest episode of Predictable B2B Success, offering his extensive expertise in public accounting and financial leadership to help you effectively sustain and scale your business.

Tune in here to check out the full episode.

Or, read on for more insights about how to use key financials to drive growth.

Exceeding Customer Expectations: Importance of client satisfaction and retention rates.

To grow your business, it’s crucial to not just meet but exceed customer expectations. Here’s why focusing on client satisfaction and retention is so important:

Why Client Satisfaction Matters

- Loyal Clients: Satisfied customers are more likely to stay with you and make repeat purchases, leading to steady revenue.

- Positive Referrals: Happy clients will share their positive experiences, bringing in new customers through word-of-mouth.

- Lower Costs: Retaining existing clients is often cheaper than acquiring new ones, saving you money in the long run.

How to Boost Client Satisfaction

- Understand Their Needs: Regularly collect and act on client feedback to better meet their needs.

- Provide Excellent Service: Train your team to be responsive and helpful in every client interaction.

- Show You Care: Make improvements based on client feedback to build trust and show that you value their input.

The Importance of Retention Rates

- Build Loyalty: High retention rates mean longer-term relationships and loyal clients who are less likely to switch to competitors.

- Increase Revenue: Retained clients are more likely to buy additional products or services from you.

Focusing on exceeding client expectations and improving satisfaction and retention helps set your business up for sustained success and growth.

Bonus Plans and Business Success: Linking Incentives to Performance

To drive business success, it’s important to align your bonus plans with your company’s performance. Here’s how linking bonuses to business goals can benefit your business and the role consistent contracts play in this process:

How Bonus Plans Drive Business Success

- Align Goals: Linking bonuses to specific business performance metrics ensures that employees’ goals are aligned with the company’s objectives. When employees know their bonuses depend on meeting targets, they’re more motivated to work towards achieving those goals.

- Reward Performance: Effective bonus plans reward employees for their contributions to business success. This can lead to increased productivity, higher quality of work, and overall better performance from your team.

- Foster a Success-Driven Culture: When bonuses are tied to performance, it creates a culture focused on achieving results. Employees at all levels are encouraged to contribute to the company’s success and are recognized for their efforts.

The Impact of Consistent Contracts

- Clear Financial Planning: Consistent contracts help maintain clarity in financial planning and forecasting. When contracts are stable and predictable, it’s easier to manage cash flow and allocate resources effectively.

- Accurate Business Valuation: Regular and consistent contracts contribute to a more accurate valuation of your business. Investors and buyers look for stability in revenue streams, and consistent contracts provide a clear picture of your financial health.

- Easier Accounting: Standardized contracts simplify accounting processes. They make it easier to track revenue, manage expenses, and prepare financial statements, reducing the risk of errors and ensuring more reliable financial reporting.

By linking bonus plans to business performance and maintaining consistent contracts, you create a more motivated team and a stronger, more predictable financial foundation for your business.

Credible Financial Information During Due Diligence: Why Accuracy Matters

When undergoing due diligence, having accurate and credible financial information is crucial. Here’s why it’s important and how it helps avoid discounted offers:

The Importance of Accurate Financial Information

- Build Trust: Providing accurate financial data helps build trust with potential buyers or investors. It shows that you are transparent and have nothing to hide, which can make them more confident in their decision.

- Avoid Discounted Offers: Inaccurate or incomplete financial information can lead to undervaluation of your business. Buyers or investors may assume higher risks and offer lower prices if they see discrepancies or unclear data.

- Smooth Negotiations: Clear and precise financial information simplifies the negotiation process. When everything is transparent and well-documented, it’s easier to justify your business’s value and secure fair offers.

How to Ensure Credibility

- Maintain Accurate Records: Regularly update and review your financial records to ensure accuracy. This includes financial statements, tax returns, and other key documents.

- Use Professional Services: Work with accountants or financial advisors to audit your financial information. Their expertise can help identify and correct any issues before they become problems.

- Prepare for Scrutiny: Be ready for detailed reviews by potential buyers or investors. Ensure that all financial data is organized and easily accessible for due diligence.

By ensuring that your financial information is accurate and credible, you can avoid discounted offers and present your business in the best possible light during due diligence.

Hiring and Processes for Success: Building a Strong Team and Effective Operations

Success in any business relies heavily on hiring the right people, implementing effective processes, and maintaining regular communication. Here’s why these elements are crucial for your business:

The Importance of Hiring the Right People

- Fit with Company Culture: Hiring individuals who align with your company’s values and culture helps create a positive work environment. Employees who fit well with the company culture are more likely to be engaged and productive.

- Skills and Experience: The right hires bring the necessary skills and experience to the table, which can drive your business forward. Properly skilled employees can contribute more effectively to achieving business goals.

- Reduced Turnover: Investing time and effort in finding the right candidates helps reduce employee turnover. Hiring well increases job satisfaction and reduces the costs associated with hiring and training new staff.

The Role of Implementing Effective Processes

- Streamline Operations: Well-defined processes ensure that tasks are completed efficiently and consistently. This helps minimize errors and improves overall productivity.

- Improve Quality: Standardized processes help maintain high-quality standards across all operations. Consistency in processes leads to better outcomes and customer satisfaction.

- Enhance Accountability: Clear processes make it easier to track progress and hold team members accountable for their responsibilities. This helps ensure that everyone is working towards common goals.

The Need for Regular Communication

- Foster Team Collaboration: Regular communication keeps everyone on the same page. It encourages collaboration and ensures that team members are informed about goals, updates, and changes.

- Address Issues Promptly: Open lines of communication help identify and resolve issues quickly. It allows for timely feedback and problem-solving, which is essential for maintaining smooth operations.

- Boost Morale: Regular communication helps build trust and strengthen relationships within the team. It keeps employees engaged and motivated, leading to a more positive and productive work environment.

By focusing on hiring the right people, implementing effective processes, and maintaining regular communication, you lay the foundation for a successful and well-functioning business.

Processes for Scaling Business Operations: Key Steps for Managing Growth

As your business grows, having solid processes in place for accounting, invoicing, bill payments, and financial reporting becomes crucial. Here’s a look at the essential processes you need to scale effectively:

1. Efficient Accounting

- Use Accounting Software: Invest in reliable accounting software to streamline financial management. This helps with tracking expenses, managing payroll, and generating financial statements.

- Regular Reconciliation: Frequently reconcile your accounts to ensure accuracy. This involves comparing your records with bank statements to catch any discrepancies early.

- Financial Controls: Implement controls to prevent errors and fraud. This includes segregating duties so that no single person handles all aspects of financial transactions.

2. Streamlined Invoicing

- Automate Invoicing: Use invoicing software to automate and simplify the billing process. Automated systems can send out invoices, track payments, and follow up on overdue accounts.

- Clear Terms: Establish clear payment terms and include them in all invoices. Specify due dates, payment methods, and late fees to avoid confusion and ensure timely payments.

- Consistent Follow-Up: Regularly follow up on outstanding invoices. Set reminders for overdue accounts and establish a procedure for handling late payments.

3. Effective Bill Payments

- Timely Payments: Set up a schedule for paying bills to avoid late fees and maintain good relationships with vendors. Prioritize payments based on due dates and contractual obligations.

- Approval Processes: Implement an approval process for bill payments to ensure that all expenses are reviewed and authorized before payment. This helps prevent unauthorized or incorrect payments.

- Track Expenses: Maintain a detailed record of all payments and expenses. Use your accounting software to track and categorize these transactions for better financial management.

4. Accurate Financial Reporting

- Regular Reports: Generate financial reports regularly, such as monthly or quarterly. These reports provide insights into your business’s financial health and help with strategic planning.

- Key Metrics: Focus on key financial metrics like cash flow, profitability, and expenses. These metrics are essential for understanding your business’s performance and making informed decisions.

- Compliance: Ensure that your financial reporting complies with accounting standards and regulations. This helps avoid legal issues and ensures transparency in your financial practices.

By implementing these essential processes for accounting, invoicing, bill payments, and financial reporting, you can manage growth more effectively and maintain a strong financial foundation as your business scales.

Financial Education for Business Leaders: Why It Matters

- Understanding Financial Basics: Business leaders, including those in marketing, sales, and customer service, need to grasp basic financial concepts. This knowledge helps them make informed decisions that align with the company’s financial goals.

- Enhancing Decision-Making: Financial education enables leaders to analyze budgets, forecast revenues, and understand financial reports. This insight supports better strategic decisions that drive business success.

- Aligning Teams with Financial Goals: When all team members understand financial principles, they can align their efforts with the company’s financial objectives. This alignment boosts overall performance and contributes to achieving business goals.

- Improving Communication: Financial literacy helps leaders communicate more effectively with financial teams and stakeholders. It ensures that financial data is interpreted accurately and used to drive meaningful actions.

Post-COVID Business Challenges: Navigating the New Normal

- Managing Cash Flow: Post-COVID, many businesses face cash flow issues due to fluctuating revenues and increased expenses. Implement strategies to monitor and manage cash flow effectively to maintain stability.

- Adapting to Uncertainty: The pandemic has increased market uncertainty. Develop flexible business plans that can adapt to changing conditions, and create contingency plans to address potential challenges.

- Revisiting Financial Strategies: Reassess your financial strategies to account for new realities. This includes revising budgets, exploring cost-saving measures, and adjusting investment plans to align with current conditions.

- Embracing Remote Work: The shift to remote work requires updated financial and operational strategies. Ensure your systems support remote collaboration and adjust financial plans to accommodate any changes in operating costs.

Technology and Data Understanding: Laying the Groundwork

- Understanding Data Foundations: Before investing in new technology, it’s crucial to understand your current data and how it’s managed. Proper data management ensures that new technology will integrate smoothly and be effective.

- Evaluating Technology Needs: Assess what technology is necessary based on your data needs. Invest in tools that will enhance data accuracy, reporting capabilities, and overall business operations.

- Data Security: Ensure that your data management practices and technology investments include robust security measures to protect against data breaches and cyber threats.

- Training and Adoption: Provide training for your team to effectively use new technology. Ensuring that everyone understands how to leverage these tools will maximize their benefits and improve business performance.

Remote Work Model and Team Investment: Adapting to a New Work Environment

- Shifting to Remote Work: The remote work model has become more common. Adapt your business operations to support remote work, including investing in collaboration tools and ensuring cybersecurity.

- Reinvesting in Team Culture: Even in a remote environment, it’s important to maintain a strong team culture. Invest in virtual team-building activities and regular check-ins to keep morale high and foster team cohesion.

- Supporting Remote Employees: Provide resources and support for remote employees to ensure they have what they need to perform effectively. This includes offering flexible work arrangements and maintaining clear communication channels.

- Evaluating Remote Work Impact: Regularly assess the impact of remote work on productivity and team dynamics. Make adjustments as needed to optimize performance and address any challenges that arise.

About Signature Analytics

Signature Analytics is a leading outsourced accounting firm providing comprehensive financial services to businesses of all sizes. With a focus on Accurate, Relevant, and Timely (ART) financial reporting Signature Analytics empowers clients to make informed decisions and achieve their financial goals. With over 16 years of industry experience and a global team of 75 professionals, the firm is dedicated to delivering excellence in accounting solutions.

Let us become your trusted partner in accounting, allowing you to focus on what you do best. Reach out to our team today to discover how Signature Analytics can support the success of your business.

For more in-depth insights from Jason Kruger and practical tips on how to use key financial strategies to drive growth, tune in here.

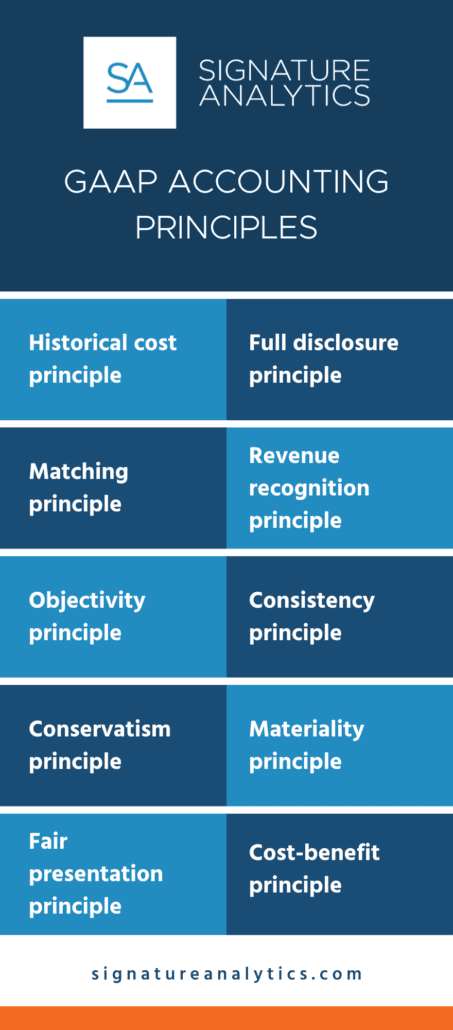

What are the principles of GAAP accounting?

What are the principles of GAAP accounting?