How to transition your business from cash to accrual accounting (and why)

Accrual vs Cash vs GAAP Accounting:

For small business owners, there is a choice to be made between cash basis accounting and accrual accounting. Larger corporations, however, are required by the IRS to utilize accrual accounting. As a business grows and passes the threshold beyond which cash-based accounting is practical it is important to transition to accrual accounting. That process is no small feat and can cause businesses to have some eye-opening financial discoveries. The fact is, that managing financials on a cash basis, can cause business owners to inadvertently deceive themselves. If your business is still using a cash-based accounting method, read on from the steps you’ll need to take to transition to accrual, why you need to do it sooner than later, and how Signature Analytics can help.

Accrual Basis Accounting

When using accrual accounting, revenue is spread out over the period in which a service is provided. Accrual accounting provides a more precise understanding of a business’ current financial picture, allowing business owners to make more informed decisions. Expenses are reflected as they are incurred, as opposed to when cash is disbursed. Therefore, short-term fluctuations in cash flow do not dramatically alter the overall financial picture.

Accrual accounting is the recommended method for almost all businesses. This method allows you to track revenues and expenses in order to assess the profitability of your business and identify trends in performance. It provides a more reliable measure of Gross Margins, giving you the insight needed to make educated business decisions. Cash accounting may appear simpler, but accrual accounting is by far the superior choice.

Cash Basis Accounting

Cash accounting is a method of bookkeeping that records transactions as they occur, rather than when revenue or expenses are actually earned. When using cash accounting, revenue from services rendered in April, May, and June will not be reflected in the financial statements until payment is received in July. This can create a false impression of business decline, despite services having been performed and earned in the prior months. This method of accounting can lead to misinformed decisions being made concerning staffing, pricing, ordering, and many other key decisions a business owner must make. To ensure accurate financial reporting, it is important to understand the differences between accrual and cash accounting.

Can a business use cash basis accounting and still be GAAP compliant?

Cash basis accounting is not GAAP-compliant. GAAP (Generally Accepted Accounting Principles) is a set of standards and guidelines for financial reporting that are widely recognized and accepted as the authoritative standard for financial reporting in the United States.

Cash basis accounting is a simplified method of accounting that only recognizes transactions when cash is received or disbursed. While cash basis accounting is simpler and easier to use, it does not provide as much information about the financial performance and position of a business as accrual accounting.

A business using cash basis accounting must still follow certain principles and guidelines, such as ensuring that transactions are recorded accurately and in a timely manner, and providing accurate financial statements that reflect the financial position of the business.

For most businesses, especially those with complex financial operations, accrual accounting is the preferred method of accounting as it provides a more complete and accurate picture of the financial performance and position of the business.

While it is possible for a business to use cash basis accounting, the limitations of cash basis accounting may result in less accurate and less informative financial statements, and most businesses may find accrual accounting to be a better choice for their financial reporting needs.

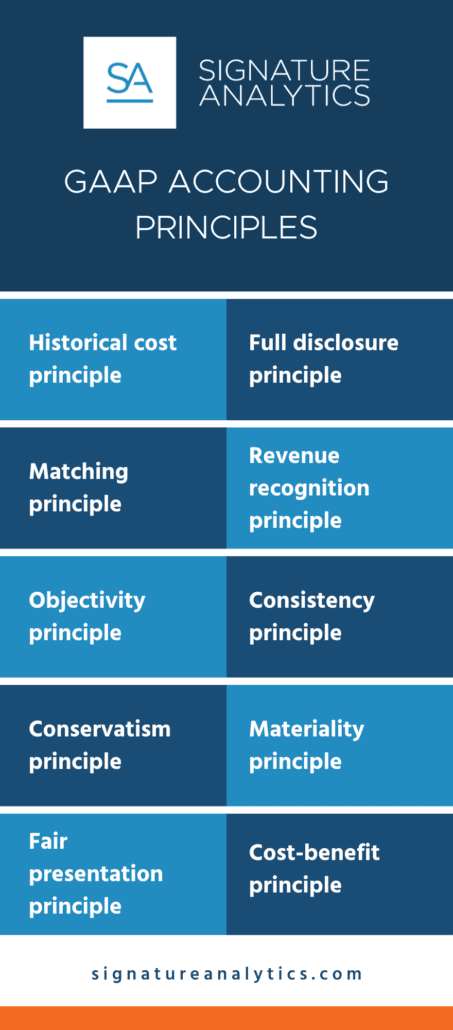

What are the principles of GAAP accounting?

What are the principles of GAAP accounting?

- Historical cost principle: Assets and liabilities are recorded at their original cost.

- Full disclosure principle: All relevant and material information should be disclosed in the financial statements.

- Matching principle: Expenses should be matched with revenues in the period in which they were incurred.

- Revenue recognition principle: Revenue should be recognized when earned, regardless of when payment is received.

- Objectivity principle: Financial statements should be based on objective evidence.

- Consistency principle: Companies should use the same accounting methods from one period to the next.

- Conservatism principle: In case of uncertainty, the financial statement should reflect the worst-case scenario.

- Materiality principle: Only information that is significant enough to affect the decisions of users should be included in the financial statements.

- Fair presentation principle: Financial statements should be presented in a way that is not misleading.

- Cost-benefit principle: The benefits of providing information should outweigh the costs.

What steps should a business take to transition from cash basis to accrual basis accounting?

Transitioning from cash basis to accrual basis accounting can be a significant change for a business, but it can also provide greater insight into the financial performance and position of the company.

Here are the steps a business should take to make the transition:

Assess your current accounting system: Review the current accounting system to determine what changes need to be made in order to transition to accrual accounting. This may involve upgrading the accounting software, hiring additional staff, or contracting with an outsourced accounting firm.

Train staff: All staff members involved in the accounting process should be trained on the new accounting methods and procedures. This will ensure that everyone is using the same methods and that the transition goes smoothly.

Implement new processes: Establish new SOPs for recording and tracking financial transactions under accrual accounting. This may include tracking accounts payable and accounts receivable and inventory differently now that you’re using an accrual method.

Review financial statements: Ensure that your financial statements are accurate and reflect the financial position of the company under accrual accounting. If necessary, make adjustments to the financial statements to ensure that they are accurate.

Monitor results: Monitor the results of the transition to accrual accounting and make any necessary adjustments. This may involve modifying procedures or making changes to the accounting software, having more regular leadership meetings to align on the meaning of financial reports, or bringing in a fractional CFO business advisor to help guide the leadership in their understanding of the numbers.

Seek professional guidance: Consider seeking the guidance of an outsourced accounting firm to ensure that the transition is successful and that the financial statements are accurate, relevant, and delivered in a timely fashion.

Transitioning from cash basis to accrual basis accounting can be a complex process, but it can provide infinitely greater insight into the financial performance and position of your company. By following the steps outlined above, a business can make the transition smoothly and effectively.

Call our expert outsourced accounting consultants today to see how we can help your business be efficient, effective and make smart decisions.