Your Guide To The Main Street Lending Program

This article was originally published on 6.11.20 and contains the new program guidelines that were released on 6.8.20. We will continue updating as new information becomes available.

During the last few months, the Coronavirus has created an incredible impact on the world. As a result of this unforeseen occurrence, many individuals and businesses were negatively affected and continue to struggle today.

The Federal Reserve announced in April that a new lending program was in the process of being established for small and medium-sized businesses that were financially stable pre-pandemic. The creation was a result that stemmed from the CARES Act as an avenue to make $600 billion accessible in aid. It complements the aid available through the Small Business Association and other funding options.

Below, we breakdown the essential facts of the program, as well as answer some commonly asked questions our team of experts is receiving. This breakdown includes the newly released guidelines from the Federal Reserve that were announced on 6.8.20.

“Supporting small and mid-sized businesses so they are ready to reopen and rehire workers will help foster a broad-based economic recovery,” Powell said in Monday’s announcement. “I am confident the changes we are making will improve the ability of the Main Street Lending Program to support employment during this difficult period,” Fed Chairman Jerome Powell recently said of the revamped program.

We hope this will serve as a starting point to understanding the plan, but in no way should one financial leader opt to manage all of this information for their business on their own. You can call our expert financial team at any time so we can help you throughout this process. Continue reading for all of the insights.

Start the ConversationWhat Is The Main Street Lending Program?

As mentioned above, the Main Street Lending program is the government’s additional solution to providing funding for small and mid-sized businesses.

The program operates through three facilities:

- Main Street New Loan Facility (MSNLF) (link to 6.8.20 term sheet)

- Main Street Priority Loan Facility (MSPLF) (link to 6.8.20 term sheet)

- Main Street Expanded Loan Facility (MSELF) (link to 6.8.20 term sheet)

For information regarding each of these facilities and answers to questions on the terms and conditions, please visit the Federal Reserve resource here.

Other key takeaways from the Main Street Loan Program update:

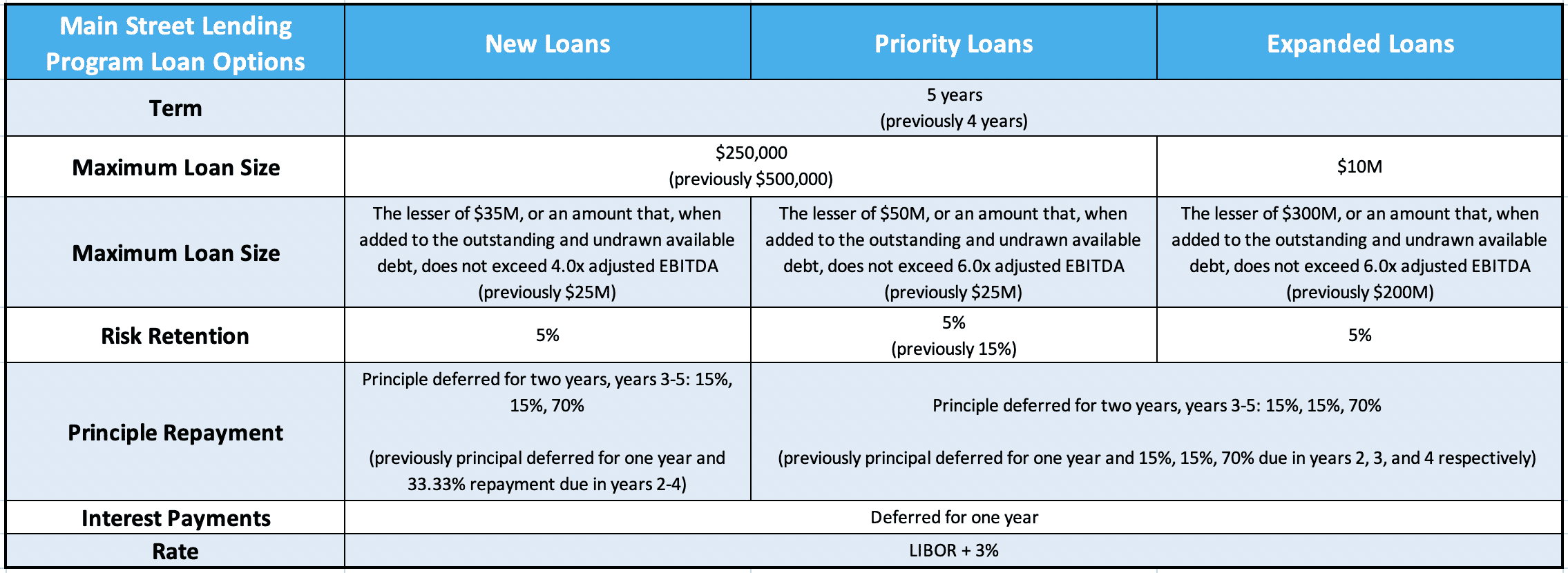

The federal research expanded its Main Street Loan Program with a few major changes to allow more small and medium-sized businesses to be able to receive support. The changes include:

- Lowering the minimum loan size for certain loans to $250,000 from $500,000.

- Increasing the maximin loan size for all facilities (Maximums for each type will be $35 million, $50 million, and $300 million). Loan caps are based on outstanding credit and adjusted EBITDA of the borrower.

- Increasing the term of the loan option to 5 years, from 4 years.

- Extending the repayment period for all loans by delaying principal payment for 2 years, rather than 1 year.

- Raising the Reserve Bank’s participation to 95% for all loans.

The Fed says the facility will open registration to potential lenders “soon.” More details can be found on the Federal Reserve website.

How Do I Know If I Am Eligible?

To participate in the Main Street Lending Program, a borrower must meet the list of criteria below. Most importantly, the business that is attempting to securing the loan must have an establishment date before March 13, 2020, and be based within the United States.

Secondly, eligibility requirements also include having either:

- less than $5 billion in 2019 revenues or

- less than 15,000 employees.

Non-profit applications should note that a separate program is in the works for their unique circumstances.

A few more eligibility details of importance include:

- being a partnership, limited liability company, corporation, association, trust, cooperative, a joint venture (with no more than 49 percent participation by foreign entities); or a tribal business concern

- not being an “Ineligible Business” under the Small Business Administration (SBA) definition, as applied to the Paycheck Protection Program (PPP)

- not participating in the Primary Market Corporate Credit Facility or receive specific support provided by the CARES Act made available to air carriers and businesses critical to national security

If your business has applied for or already received Paycheck Protection Program (PPP) funds, the Federal Reserve has made it clear these do not make a business ineligible for a loan from the Main Street Lending Program.

How Do I Apply For The Program?

Business leaders can visit or call any U.S. bank to apply for a Main Street Lending program loan. It may be easiest to select where you already have established your banking relationship; however, there are no restrictions.

The bank you choose to work with will first assess the risks and then will offer you an interest rate. Our recommendation is to apply with two separate banks and make your selection based on the most competitive interest rate you are offered. Since bank lenders are now only required to take on 5% of the loan, more competitive rates will become available.

It is important to note that there will be fees associated with your loan, so understanding this upfront can help you make your final decision.

Is There A Limit or Minimum To How Much Aid I Can Borrow?

Yes, there are restraints on how much a business can borrow. Loans offered through the Main Street Lending Program range from $250,000 to $300 million.

Depending on the type of loan, each will have a 5% to 15% risk retention rate. What this means is that for banks, they are guaranteed in this amount by the federal government.

What Else Should I Know About The Program?

We cannot stress this enough, but once you receive your funding and in your account, there is no separation between those funds and your other finances. With that, it is critical to use a tracking method, so you have documentation of where the funds are allocated.

Two Tips From Our Expert CFO’s

Here are two questions to ask yourself or your company’s financial leaders:

- Have you developed a 13-week cash flow plan? Even better if you can create a plan through the end of the year. Having this type of cash flow forecast will allow you to plan for all revenue and expenses while still providing visibility to make strategic decisions.

Read More: Actionable Advice from Our Founder to Improve Your Cash Flow - Have you gone through the appropriate steps for scenario planning? You likely need assistance projecting your cash needs, figuring out potential profitability, and determining how best to make data-driven decisions. Using the scenario planning model, you can forecast your business results over an extended period.

Read More: Your Guide To Financial Modeling And Scenario Planning for COVID-19

If the answer to either of these questions is no, now is the time to get started. We are asking our clients to develop and execute these plans to help them plan for their future as much as possible.

Our CFO team is already supporting these initiatives and are happy to help you dive deeper into the best decisions for your company using limited resources.

Do Not Navigate This Alone

There are many programs designed to help businesses impacted by COVID-19, and this is only one of them. As a business leader, you are a decision-maker in your company, and you must be armed with accurate information to lead your company to success.

You can call us with any questions you have or advice you are looking for while navigating the Main Street Lending program or other programs out there. We also work with a number of banks that are part of the lending program. It is our promise to go beyond the numbers to help improve your business performance and achieve your goals. Our team of experts is ready to help you lead your business into the new normal with funding in your bank account.

Talk to An Expert