A Summary: Coronavirus Aid, Relief, and Economic Security (CARES) Act

This article was originally written on April 8 and portions have been updated on July 7, 2020. The following information is what we know to be accurate, and it is very likely new information will evolve over time as we learn intricate details of this bill. We will continue to update this article as we learn more.

On March 27, 2020, S.3548 the Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law to give emergency assistance and health care response for individuals, families, and businesses affected by the 2020 coronavirus pandemic.

As the most massive stimulus bill in American history ($2.2 trillion), it includes several relief areas for individuals and businesses including:

- Direct payments to tax-paying Americans

- Enhanced unemployment aid

- Small business loans and grants

- Loans for the airline industry and other big businesses

- Money for individual states, hospitals, and education systems

- Tax cuts

- An increase in safety net spending

- A temporary ban on foreclosures

Read the entire bill in all of its detail here.

There are some aspects of this bill that will directly affect our customers and their businesses, which we have broken down in detail below.

Start the ConversationDirect Payments To Tax Paying Americans

Part of the $2.2 trillion of aid this bill brings includes an estimated $290 billion set aside for payments to the American people. Citizens who pay taxes are reported to receive a direct payment from the U.S. government. The amounts of those direct payments vary based on household size and income level. These figures are represented below:

- Single individuals are expected to receive a one-time payment of $1,200

- Married couples are expected to receive a one-time payment of $2,400

- Families with children under the age of 17 are expected to receive an extra $500 per child.

There are some stipulations for these monetary amounts. Those are for Americans earning more than $75,000 per year, the number of direct payments may be lower. Individuals earning more than $99,000 per year are not eligible for these payments. Another important note is one that affects child support payments. If an individual is behind on child support payments, they will not be eligible for this direct payment.

Small Business Payroll Protection Program

The CARES Act should also help many small companies and 501(c)(3) nonprofits who have suffered from little-to-no business during the COVID-19 pandemic.

Through the Payroll Protection Program (PPP), businesses with less than 500 employees have the ability to secure loans up to 2.5 times the average months of its payroll costs or up to $10,000,000.

If a small business, with employees located in the United States, were to secure this loan, they could use it to help cover some of the following needs:

- Salaries

- Rent

- Healthcare benefits

- Debt obligations

- Mortgage interest

- Utility costs

It should be noted that securing a loan under the PPP can only cover expenses from February 15 to June 30. There is an estimated allocation of $350 billion set aside for loans and emergency grants.

If you think your small business or nonprofit organization could capitalize on this opportunity, call your Small Business Administration lender to begin the process as soon as possible. If you are not sure who your SBA lender is, start by contacting your local banks within your area or try the SBA Eligible Lender locator found here.

Read More: Planning and Managing Your Banking Relationship During COVID-19

It might take some time to organize essential information like tax records and other important documents. The sooner all of these items are organized, the sooner the loan will come through. Be aware the first day to apply for these loans is April 3, 2020.

To help you get started, here are some great resources from the U.S. Treasury office:

- Paycheck Protection Program (PPP) Application

- Paycheck Protection Program (PPP) Fact Sheet

- Information on Paycheck Protection Program (PPP)

For more information and details on the PPP (there are a lot of them), but the above resources can help you get started right away. Continue checking our internal resource center under the “Employer Resources” tab. Additionally, there are many on-demand webinars that can provide additional insight.

As always, do not hesitate to reach out to us for assistance.

Read More: COVID-19 Resource Center

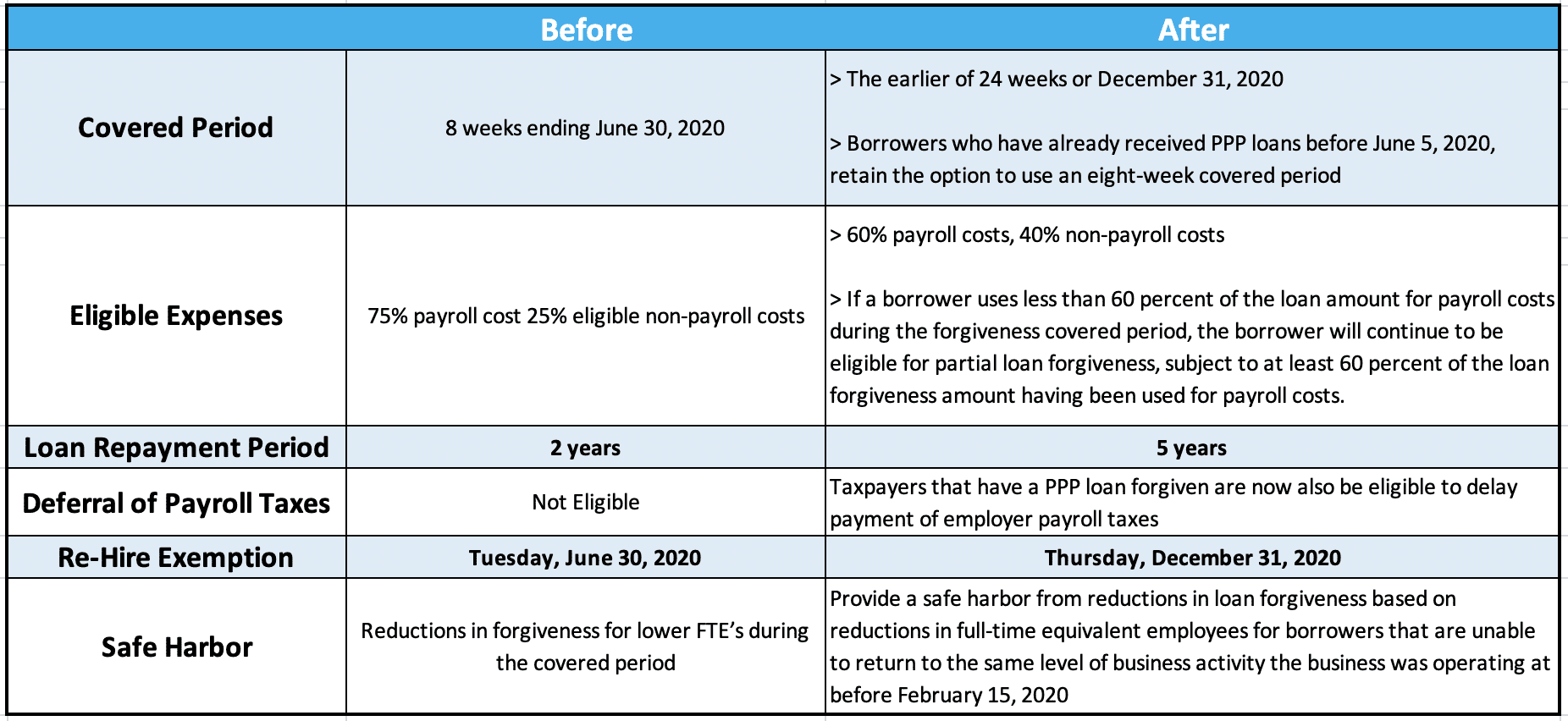

Paycheck Protection Program Flexibility Act of 2020: Amendments to the PPP

On June 5, 2020, President Trump signed into law the PPP Flexibility Act, with amendments to the previous PPP.

Below we have outlined the main takeaways to help you understand the most significant changes.

- The new legislation alters the existing PPP, giving borrowers more time to spend loan funds with the ability to obtain forgiveness.

- Loan borrowers now have 24 weeks to spend their loans.

- There is a reduction in mandatory payroll spending from a previous 75% down to 60%.

- Businesses can now delay paying payroll taxes even if they took a PPP loan.

- Borrows can now receive full loan forgiveness if they have yet to restore their workforce fully.

- The loan repayment schedule extends from two years to five years.

New updates 07.07.20:

The original (but newly released) PPP Loan Forgiveness Form was a little too complicated for smaller business owners that may not have immediate access to an accountant or lawyer, therefore, the SBA released the Paycheck Protection Program Loan Forgiveness Application Form 3508EZ. The 3508EZ Form can also be ideal for:

- the self-employed or businesses that have no employees OR

- businesses that did no reduce the salaries or wages of their employee by more than 25%; and did not reduce the number of hours of their employees OR

- businesses that experienced reductions in business activity as a result of health directives related to COVID-19 and did no reduce the salaries or wages of their employees by more than 25%.

Also, the payroll calculation used in the loan application still applies to the forgivable amount, meaning the employee compensation eligible for forgiveness is capped at $100,000. However, they are increasing the max forgiveness per employee (non-owners):

- Originally $15,384.61 for the eight-week period ($100,000 pro-rated)

- It is now $46,153.85 for the 25-week period.

For Owners, Sole Proprietors, Independent Contractors, or General Partners:

- For the 8-week period, forgiveness for owner compensation is calculated as 8 / 25 X 2019 compensation, up to a maximum of $15,385 in total for all businesses.

- For the 24-week period, the forgiveness calculation is limited to 2.5 months’ worth (2.5 / 12) of 2019 compensation, up to $20,833, also in total for all businesses.

The final day to apply for the PPP loan has been extended to August 8, 2020, allowing eligible small businesses more time to apply for the remaining $130 million of PPP lending capacity.

PPP recipients can apply early for forgiveness? We’ve had many clients ask us whether they can apply for PPP loan forgiveness before their covered period expires. By doing so, they forfeit a safe-harbor provision allowing them to restore salaries or wages by Dec. 31st and avoid reductions in the loan forgiveness they receive. So for now as things are evolving, we say hold off on doing this. Most banks will start accepting loan forgiveness applications in mid-August.

There is still much to learn about relaxing guidelines, we will do our best to keep this updated.

More Time to Spend Loan

One of the most significant changes with the PPP Flexibility Act is now borrowers have more time to spend the amount of their loan. Previously, only eight weeks were allotted to spend this money, which put a considerable amount of pressure on the borrower to ensure the funds were spent on forgivable expenditures. The time frame has been increased to 24 weeks after the origination of the loan or to December 31, 2020, whichever is earlier.

Payroll Spending

A reduction has been made to the mandatory payroll spending. This means the amount of money from the loan that was required to go toward payroll costs has been reduced from 75% to 60%.

What this change allows is for forgivable non-payroll expenses to be as high as 40%, enabling small business owners to put that money toward other costs they were struggling to pay. For example, for businesses that covered their payroll costs but still didn’t have enough to pay bills like rent, this helps free up some of the money for this purpose.

Repayment Period

The repayment period has been extended. Previously, the repayment period was for two years, and now the extension goes to five years while retaining a 1% interest rate. Ultimately, this allows borrowers extra time to pay off the unforgiven portion of their loan.

If a borrower received their loan prior to June 5, 2020, there is a 2-year maturity. If the loan was made after this date, it has a five-year maturity.

Would you like to read the new law? You can access it through congress.gov here.

Tax Cuts For Businesses

One of the other significant aspects of the CARES Act is the tax cuts for businesses. There have been modifications made to the Tax Cuts and Jobs Act (TCJA) of 2017. These modifications directly affect the net operating loss rule, lifting the 80% rule, and ensuring losses are carried back five years.

There is other positive news for businesses and their payroll. A refundable 50 percent payroll tax credit for businesses directly affected by the novel Coronavirus is available to help employee retention.

A few other areas of significance include:

- Any distilleries who are helping to create hand sanitizer in their facilities will have federal tax waived

- Businesses are able to write off donations of goodwill and student loan payments for their employees

- Suspension of penalties for those who must tap into their retirement funds

Every business finds itself in a unique situation during this time; therefore, if you are not already partnered with us, we recommend that you work with a tax CPA or Small Business Administration lender on how to navigate this bill and how it impacts your company.

Signature Analytics is here to support you and can provide references to our partner network upon request. Feel free to contact us to get started.

New Updates For Consideration

It is important to understand the CARES Act is on a “first-come, first-serve” basis, so if your organization needs funding, we urge you to get your paperwork submitted as quickly as possible.

- Based on how many employees you have, the limit used when calculating payroll costs is $100,000 and includes insurance, benefits, and taxes.

- Eligibility for PPP for self-employed or independent contractors is based on self-employment net income, but cannot be counted for payroll costs.

- Any federally illegal businesses will not receive funding and cannot participate in this program.

*updated 06.08.20

Talk to An ExpertNearly $500 Billion More In Aid

As of the evening of April 21, the Senate has approved $484 billion in aid for the stimulus package. On April 23, the bill will go to the House to pass as a complete package and make this funding available.

This additional funding is to support the small businesses, hospitals, and many other businesses negatively impacted by the coronavirus. However, $310 billion of this aid is considered being allocated for the Paycheck Protection Program, $60 billion of which will likely be set aside for smaller lending facilities and credit unions.

Under the emergency Economic Injury Disaster Loan program, there should be roughly $410 billion in grants, $50 billion for disaster recovery loans, and 42.1 billion for salaries and other expenses for the SBA.

Hospitals and health care providers are looking at a likely $75 billion and an additional $25 billion for COVID-19 testing.

All of these amounts are part of what the House will take into consideration later this week.

Resources:

https://www.forbes.com/sites/leonlabrecque/2020/03/29/the-cares-act-has-passed-here-are-the-highlights/#c2e55d268cd2

https://www.reuters.com/article/us-health-coronavirus-usa-bill-contents-idUSKBN21D2CQ

https://www.cpapracticeadvisor.com/tax-compliance/news/21131709/summary-of-the-coronavirus-aid-relief-and-economic-security-cares-act

https://taxfoundation.org/cares-act-senate-coronavirus-bill-economic-relief-plan/

https://www.congress.gov/bill/116th-congress/senate-bill/3548/text

https://www.cohnreznick.com/insights/sba-amends-requirements-for-its-paycheck-protection-program